June 23, 2026. South Korea's KOSPI fell nearly 10% in a single day, triggering its fourth circuit breaker of the year. Overnight, U.S. megacap tech stocks also weakened, while the memory leader hit a record intraday before fading in after-hours trading. Both markets came under pressure on the same day, reviving questions about whether the AI rally has peaked—or even crashed. But whether markets crash depends not on sentiment, but on the numerator and denominator of valuations. This note goes through what happened first, then why, and finally uses the valuation framework to offer an open-ended conclusion.

First, the news: what actually happened today

In one sentence: Korea went from "coronation" to circuit breaker in a single trading session; the U.S. saw profit-taking in megacaps, with memory surging against the trend before fading after-hours. What both markets share is a crowded trade loosening ahead of Micron's earnings.

1.1 Korea: a one-day reign at the top, followed by a near-10% circuit-breaker plunge

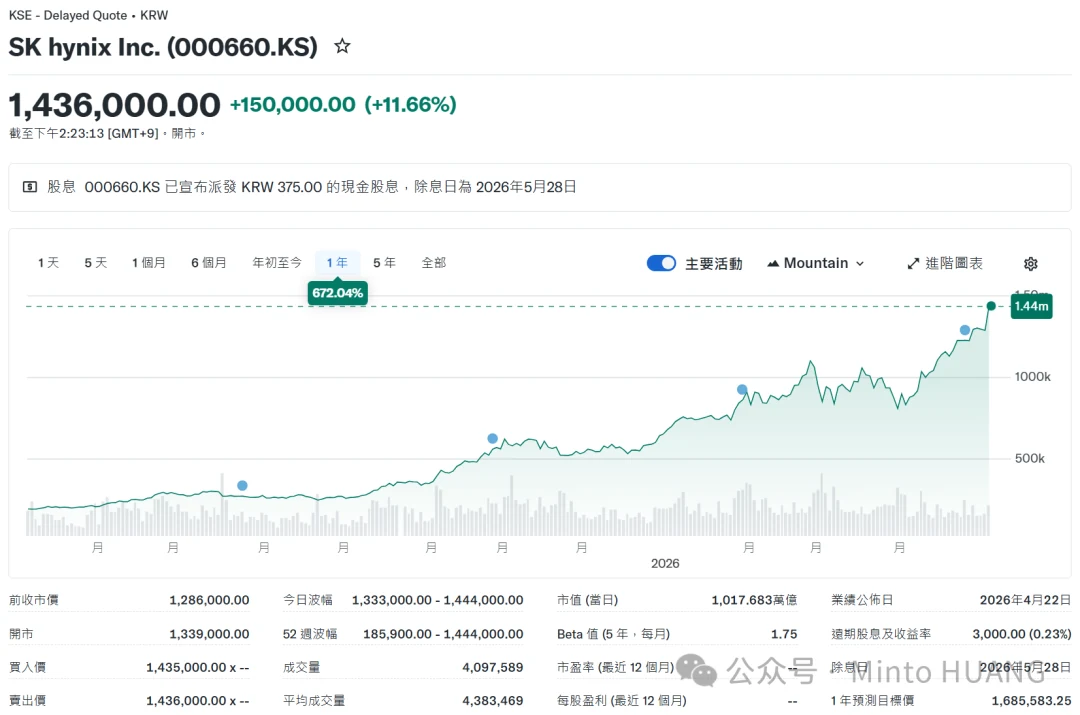

The tension lies in the 24-hour swing. On June 22, SK Hynix closed up 5.61% at KRW 2,919,000, with a market cap of KRW 2,080 trillion, surpassing Samsung Electronics' KRW 2,066 trillion (excluding preferred shares)—the first time in 25 years and 7 months a company other than Samsung topped the single-stock cap ranking. Including Samsung's KRW 179 trillion in preferred shares, the combined Samsung entity was still larger at KRW 2,246 trillion, so the coronation was always partly symbolic.

On June 23, the script flipped. The KOSPI opened lower, tried to rebound, then turned sharply down, closing at 8,203.84, down 910.71 points or 9.99%—the largest point drop in history. During the session, both KOSPI and KOSDAQ triggered sell-side circuit breakers, marking the fourth such event this year. Samsung Electronics and SK Hynix each plunged about 12%, together wiping out roughly KRW 520 trillion in market value. Samsung, helped by being comparatively less hammered, reclaimed the top spot. Hynix's reign lasted exactly one day.

A structural point: Samsung Electronics, Samsung preferred shares, SK Hynix, and SK Square together account for close to 60% of the KOSPI's weighting. So the index's near-10% drop today is essentially the profit-taking in a single sector—semiconductors—amplified by index weighting, not a simultaneous deterioration across the entire market.

1.2 U.S. megacaps: profit-taking in hyperscalers, memory hit a high before fading after-hours

Overnight in the U.S., the divergence was telling. On one side, megacap tech weakened: the Nasdaq Composite fell 1.32% on June 22 to 26,166, with the Magnificent Seven broadly under pressure, led lower by AI hyperscalers amid renewed questions about capital expenditure sustainability. On the other side, memory surged against the trend: Micron rose on the back of a strategic deal with Anthropic announced on June 22, plus a wave of target price upgrades (Bernstein raised its target 155%, and three other analysts doubled theirs), hitting a 52-week high of roughly $1,213 intraday.

But after the spike, the first crack appeared. Micron fell about 2.7% in after-hours trading, catalyzed by profit-taking ahead of its earnings and by tech investor Dan Niles publicly cutting his semiconductor position, warning that the AI trade faces a short-term "speed bump." In the prior two weeks, Micron had already rallied 40.2%. In other words, the memory leader was entering its earnings report perched at a parabolic high, supported by a single company-specific catalyst.

The table below puts today's sell-off in context.

| Market / Ticker | Today's Performance | One-Line Note |

|---|---|---|

| KOSPI | Close -9.99%, largest point drop ever | Fourth circuit breaker this year; semiconductor weight amplified |

| Samsung Electronics / SK Hynix | Both -~12% | Combined -~KRW 520 trillion market cap; Samsung retakes top |

| Nasdaq Composite | June 22 -1.32% | Magnificent Seven weak; AI spending fears lead |

| Micron (MU) | Intraday record ~$1,213; after-hours -~2.7% | Anthropic deal boosted; profit-taking gave back |

Second, why today, and why together?

The direct trigger is crowded trade profit-taking ahead of Micron earnings; the structural trigger is the first serious question about AI capex sustainability; the backdrop is a hawkish Fed and falling oil prices. All three combine, but none point to a real collapse on the earnings side.

2.1 Direct trigger: crowded trade meets a pre-earnings sentiment vacuum

The simplest explanation is crowding. On June 22, as Samsung and Hynix vied for the top spot, the euphoric inflow created extreme one-sided positioning. Today, foreign and institutional investors turned around and exited via profit-taking, while retail buyers couldn't absorb the selling, causing a sharp drop and elevated volatility. This is not an isolated case: Micron is referred to in Korea as the "bellwether" for Samsung and Hynix, as it is the first global memory company to report earnings. Before its after-hours report on June 24, the entire market entered a classic sentiment vacuum—good news already priced in, no one willing to chase at this asymmetric moment, so the large semiconductor stocks that had rallied the most were the first to loosen. Locally, discussion of including unrealized capital gains in Korea's comprehensive income tax added another layer of sentiment pressure.

2.2 Structural trigger: AI capex sustainability questioned for the first time

Deeper than sentiment, the demand-side narrative faced its first serious challenge. The June 22 divergence in U.S. stocks is telling: the stocks being sold were the hyperscalers that are spending on compute (Alphabet down ~10% at one point, Amazon, Oracle, Meta, Palantir all weaker), on the argument that AI capex is too high and returns are uncertain. Meanwhile, the stocks being bought were memory suppliers, the direct beneficiaries of that spending. Demand side sold, supply side bought—within one day, this was a reordering of capital within the AI chain, not an abandonment of AI as a whole.

2.3 Macro backdrop: a hawkish Warsh and falling oil prices

The backdrop had two opposing forces. One was a relief: U.S.-Iran talks made significant progress, with a peace deal possible within two months, sending oil prices lower—a net positive for risk assets in normal circumstances. The other was tightening: new Fed chair Kevin Warsh held rates steady at the June 17 FOMC meeting but removed the dovish bias, striking a hawkish tone; April PCE hit 3.8% year-over-year, the highest in three years, and May PCE is due Thursday. For high-valuation growth stocks, the latter force was more punishing. Today's sell-off occurred in a mixed backdrop of easing geopolitics but a tightening discount rate outlook.

Third, a professional lens: numerator and denominator—will it crash?

A crash takes only two shapes: a runaway discount rate on the denominator side, or earnings falsification on the numerator side. Putting today's sell-off into this framework, and adding three fuses, shows exactly how many have blown.

Splitting any company's—or market's—valuation into its simplest two sides: the numerator is earnings, the denominator is the discount rate. For stocks to crash, either the denominator must suddenly spiral out of control, crushing all high-valuation assets; or the numerator must be falsified, pulling the rug from under the story that supports the valuation. Which category today's plunge falls into determines whether it's a correction or the start of a crash.

3.1 Denominator side (rates): the discount rate is tightening, but not out of control

The denominator corresponds to the third fuse: Fed policy. The current reading is "tightening, but not out of control." Warsh removed the dovish bias, PCE returned to 3.8%, and that indeed pushed discount rate expectations up a notch, which is one root cause of high-valuation tech stocks' weakness today. But the key is that this was a shift in bias, not an actual rate hike. The denominator is raising the ceiling on valuations, but it hasn't yet created a rate shock that would blow up the whole market. As long as the Fed stays at "hawkish on hold" rather than "forced to hike," the denominator side only compresses multiples, not overturns the table.

3.2 Numerator side (earnings): hardware results and AI revenue are still expanding; cracks are in sentiment, not numbers

The numerator side corresponds to the other two fuses: megacap capex (hardware earnings) and AI lab cash flows (AI revenue). There's an easy-to-overlook causal order here: these two are not parallel but two sides of the same coin, and the real risk chain has a sequence—revenue falsification leads to ROI doubts, which lead to capex cuts, which lead to hardware earnings collapse. So AI revenue is the leading indicator for capex and should be tracked as an advance gauge.

Looking at this sequence, the numerator side is still expanding. Cracks are in sentiment, not numbers. On the capex front, aggregate hyperscaler guidance for 2026 is still around $700–$725 billion, up ~77% year-over-year; capacity is sold out through 2026; Micron's consensus EPS for the current quarter is up nearly 10x year-over-year. All this indicates that hardware orders and earnings are still accelerating, with no first-time order cuts or guidance downgrades. On the revenue front, OpenAI's ~$25–$33 billion run rate comes with high cash burn and breakeven pushed to 2030—a latent risk. But Anthropic's ~$45–$47 billion run rate, with positive free cash flow expected by 2027, plus thousands of enterprise annual contracts paid in real money, shows that underlying demand is genuine. Putting the two together, the megacaps being sold today are being sold on the worry that "spending is excessive," not on any already-deteriorating financial report. The numerator side has not been falsified.

One almost separate transmission channel in this chain is the circular financing. The market has identified over $800 billion in interlocking arrangements: Nvidia invests in OpenAI, OpenAI commits cloud capacity to hyperscalers, hyperscalers turn around and buy Nvidia GPUs. This is the pipe through which a numerator problem could infect hardware. The earliest pressure points would show not in stock prices, but in infrastructure firms' balance sheets—debt, lease commitments, and CDS spreads. A subtle shift signal already visible: Jensen Huang has said the $30 billion investment in OpenAI "might be the last" and that $100 billion is "not on the table." This is a table of leading indicators to watch, but as of today, it's still a warning, not an accident.

3.3 Scoreboard for the three fuses: roughly 1 to 1.5 are blinking now

Going back to the framework from that article: one fuse blown corresponds to a major correction, two blown to the start of a bear market, three blown to the AI trade being a valuation bubble. Reading today's price action into that framework, the scoreboard looks roughly like this:

| Valuation Component | Corresponding Fuse | Blow-up Form | Current Reading |

|---|---|---|---|

| Denominator · Rates | Signal 3: Fed | Forced hike, discount rate shock | ~0.7–0.8 (hawkish on hold, tightening but not out of control) |

| Numerator · Hardware Earnings | Signal 1: Megacap Capex | First order cut or guidance downgrade | ~0.7 (sentiment doubts heating up, but numbers not falsified) |

| Numerator · AI Revenue | Signal 2: Lab Cash Flow | Revenue falsified, ROI collapses | ~0.3 (latent; deals are actually increasing) |

Adding them up, roughly 1 to 1.5 fuses are blinking now. That's higher than the 0.5 to 1 reading a week ago after the FOMC meeting—risk temperature is rising. But it's still clearly below the threshold of "two = start of bear market." This aligns with the call for a "year of rotation" where tops occur sequentially, not simultaneously. Today's sharp sell-off in Korean memory is a sign that this "last bastion" is beginning to roll over, but its shape is profit-taking, not earnings collapse.

One more caveat for the worst case: even if all three fuses blow, given that underlying demand is real, the result would more likely be a severe repricing or a cyclical bear market, not a pure fraud-like bubble. This distinction matters for positioning, because the recovery paths are completely different.

Fourth, conclusion: not a crash, but this conclusion is not locked

The numerator is not falsified, the denominator is not out of control. Today's plunge is a repricing and profit-taking, not a crash. But this conclusion has two openings: tomorrow's Micron earnings are the next read on the numerator, and the inflation-Fed path over the coming months is the next read on the denominator.

To distill the analysis into one sentence: today's simultaneous sell-off in Korea and the U.S. is a concentrated profit-taking event in the numerator side (crowded trades) against a denominator side that is sentimentally tight, not a valuation crash. A crash requires either the numerator to be falsified or the denominator to run out of control—and as of today, both remain in "warning" territory, not "accident." So the base case is: markets will not crash.

But this conclusion is not locked; it has two clear openings, both close at hand.

First, the numerator side—tomorrow. Micron reports after the close on June 24, the first global memory company to report, and thus the first real read on hardware earnings delivery. The judgment does not rest on the headline numbers—Micron has beaten consensus for four straight quarters—but on three things: whether gross margin this quarter holds around 81%, where the Q4 fiscal revenue guide falls relative to the whisper, and the pricing and allocation language for HBM4 in 2027. A beat with an upgraded guide would dial the numerator fuse back from 0.7, extending the rally. A beat with a weak guide would be the first real crack in the numerator, and combined with an already tight denominator, could push the scoreboard toward the "two fuses" bear threshold. Given that Micron is trading at a record high, average analyst targets are 10–20% below the stock price, and it just saw Korean peers crushed, a "sell the news" outcome is a scenario to take seriously.

Second, the denominator side over the coming months. Thursday's May PCE print, and the inflation path in subsequent months, will determine whether Warsh stays at "hawkish on hold" or is forced toward actual rate hikes by inflation. The former only caps valuation ceilings; the latter would constitute a denominator shock. If the denominator moves from 0.7 to blown, combined with any numerator crack, the conclusion would need to be rewritten from "not a crash."

So more precisely: based on verifiable trigger conditions, today does not constitute a crash, but risk temperature is rising. The real watershed moments are tomorrow's Micron guidance language and the PCE/Fed choices in the coming months. Until those two readings are in, calling today's sell-off a crash is premature; calling it nothing also misses the point.

Risk warning: This content is for informational purposes only and does not constitute investment advice. Markets involve risk; invest with caution.

专注投资分析、市场洞察与资产配置。不追短期波动,只理解真正驱动长期回报的东西。