For quick reading, each analysis post will now come with a condensed version. This one compares Samsung and SK Hynix's technology and development paths in .

The Silicon Power Restructuring: Global HBM Game and Memory Economy Transition in 2026

In 2026, the global semiconductor industry is undergoing a profound paradigm shift. Memory chips have officially shed their traditional commodity cycle label, rising to become the core strategic asset that determines the ceiling of AI computing power. The epicenter of this transformation is High Bandwidth Memory (HBM), where thermal management and yield control in manufacturing are redefining the global tech landscape worth hundreds of billions of dollars.

I. The Computing Bottleneck: From the "Memory Wall" to Agentic AI Load Pressure

The core contradiction in current computing systems is the extreme imbalance between processor performance and memory bandwidth. Over the past two decades, logic performance has improved roughly 60,000-fold, while standard DRAM bandwidth has only increased a hundredfold. This "memory wall" has become particularly lethal after the explosion of Agentic AI.

Unlike earlier simple interactions, Agentic AI possesses autonomous planning and error-correction capabilities, leading to exponential growth in internal reasoning steps and data throughput. By the end of 2025, monthly AI token generation had increased nearly a hundredfold compared to 2024. HBM technology, using Through-Silicon Vias () for 3D stacking, provides bandwidth of up to 1–2 TB/s, becoming the physical foundation supporting this massive infrastructure.

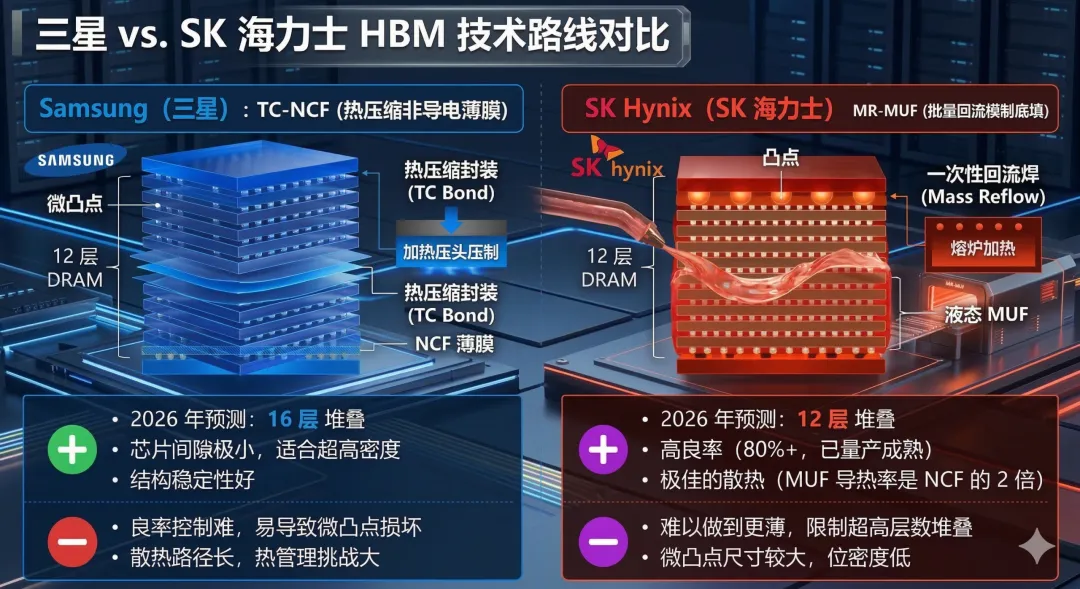

II. The Pinnacle of Process: TC-NCF vs. MR-MUF Divergence

In the era of 12-layer (12-Hi) and 16-layer (16-Hi) stacking, yield has become the dividing line between survival and failure. Two distinct technology paths have emerged:

SK Hynix, with its MR-MUF process, has overcome thermal and warpage challenges, establishing a clear advantage. Samsung, on the other hand, has hit physical bottlenecks in its transition to 16-layer stacking, making yield ramping extremely difficult.

III. The "Vampire Effect": Capacity Cannibalization and Supply Chain Bloodbath

The expansion of HBM has created a "structural squeeze" on the consumer electronics supply chain. Due to the complexity of manufacturing, producing one HBM wafer consumes resources equivalent to three standard DDR5 wafers. This 1:3 capacity cannibalization effect has led to a sharp contraction in memory supply for PCs and smartphones.

In Q1 2026, DRAM contract prices surged over 50%. As a result, memory costs now account for more than 23% of total PC bill of materials, causing global PC shipments to shrink by an estimated 11%. The valuation logic for memory stocks has also shifted dramatically: investors no longer focus on cycles but chase growth premiums, with P/E multiples expanding from the traditional 5–8x to 20–30x.

IV. Capital War: Hyperscaler Preemption and Upstream Bottlenecks

AI infrastructure in 2026 has become a cash-burning capital contest. Hyperscalers like Microsoft and Meta have pre-paid billions to lock up HBM capacity for the next two years. SK Hynix and Micron's capacity is sold out through 2027.

However, capacity expansion is constrained by extremely obscure upstream bottlenecks. For example, Japan's Nitto Boseki controls 90% of the global supply of specialty low-thermal-expansion glass cloth, a critical material for preventing warpage in high-layer HBM substrates. Additionally, delivery delays from Disco's grinding equipment and ASML's lithography machines further cap capacity upside.

V. Endgame Evolution: Geopolitics and the Future of Heterogeneous Integration

Looking ahead to the HBM4 era, the traditional IDM model is transitioning to ecosystem collaboration. SK Hynix has formed a deep alliance with TSMC, using advanced logic processes to manufacture the base die for heterogeneous integration. Samsung, leveraging its full-stack integration advantage, is attempting a comeback through hybrid bonding technology for stacking beyond 20 layers.

On the geopolitical front, memory chips have taken on national security attributes. Micron, backed by policy support, has fully exited the consumer business to focus on AI. Chinese manufacturers, under blockade, are pursuing breakthroughs through mature process innovation and domestic substrate R&D, aiming to achieve supply chain resilience.

Conclusion: The Strategic Value of the Silicon Cortex

In the silicon world of 2026, whoever masters advanced packaging and thermal management holds the throat of the global AI industry. Memory chips have officially shed their "digital oil" label, becoming the most precise, expensive, and strategically valuable silicon cortex in human history. This high-stakes gamble on physical limits and capital density will determine the global tech power structure for the next decade.

Risk Disclaimer: The views in this article are for reference only and do not represent investment advice. Market risks exist; invest with caution.

专注投资分析、市场洞察与资产配置。不追短期波动,只理解真正驱动长期回报的东西。