The Hang Seng Tech Index has been in freefall, with horror stories piling up: massive CapEx by big tech, severe cash burn, gloomy revenue outlook; fierce AI competition, with unlisted ByteDance crushing the index's heavyweights; Tencent's slow AI progress, suggesting its late-mover strategy is failing; and internal cannibalization among index heavyweights—the food delivery war has crippled Meituan, JD.com, and Alibaba. Technically, the monthly MACD has formed a death cross—the last time that happened, the index fell for three years. On the funding side, Asian allocators are shifting money to Korean stocks (Samsung, SK Hynix) for hardware certainty, Japan's Nikkei, and Taiwan's TSMC-heavy market. Hong Kong IPOs are expected to raise over HKD 1 trillion this year; two recent listings—Zhipu and Minimax—have already sucked liquidity out of the market, adding billions in market cap in weeks, surpassing many index heavyweights. Add in lock-up expirations from last year's IPOs, and the list of negatives seems endless (plus the Middle East tensions and the Strait of Hormuz blockade).

When an index falls past the psychological threshold, investors start joking darkly, calling it the "Heng Seng Food Delivery" index. This sentiment reflects a harsh reality: the index's composition has tilted heavily toward lifestyle services, and these core weights are facing cross-generational suppression from off-exchange giants like ByteDance in the 2026 competitive landscape.

This suppression is not just about the shift in traffic distribution rights but also about how capital markets redefine "platform moats." In the past, we gave giants high premiums, assuming their massive user bases made them invincible. But in the wake of the "DeepSeek moment," which democratized AI, the simple "platform rent-collection" logic is crumbling. When technology is no longer a privilege of the few and efficiency gains are shared, big tech is forced to move from comfort zones to hardcore infrastructure—a game of "blood-making."

At the same time, fundamental valuation models are undergoing unprecedented stress tests. Rumors that the preferential tax rate will revert to the standard 25% hang like a sword of Damocles, directly threatening systematic downward revisions to EPS. Driven by fiscal logic and regulatory scrutiny, the multiples that once supported stock prices are contracting sharply, explaining why this 30% decline feels so heavy and hard to recover from.

This article goes beyond technical analysis to dissect how, at this valuation inflection point in 2026, Hang Seng Tech giants are seeking a fragile balance between "zero-sum competition" and "value reconstruction" under the triple pressures of asymmetric competition, tightening fiscal policies, and the AI generational shift.

The Underlying Collapse of the Hang Seng Tech Index and Liquidity Battles

1.1 Macro Liquidity Mismatch: Rate Cuts as "Catalyst" and "China's DeepSeek Moment"

Let's rewind to two years ago, the heyday of Hang Seng Tech. In the 2025 macro narrative, the Fed's policy pivot was seen as the ultimate lifeline for the Hang Seng Tech Index (HSTECH). But as we entered the rate-cutting cycle, market feedback revealed a complex, non-linear game. While rate cuts provided liquidity room, what truly made foreign capital reassess Chinese tech stocks was the "China DeepSeek moment" that erupted in 2025 and continued to ferment.

Previously, foreign investors priced Hong Kong-listed internet stocks based on a "China consumption dividend" premium, which was questioned due to weak domestic demand between 2024 and 2025. However, the global leap in "inference cost" and "algorithm efficiency" achieved by models like DeepSeek completely reshaped foreign perceptions. This was no longer a simple "Copy to China" but a "high-efficiency infrastructure's dimensionality reduction strike on global computing power."

Foreign investors realized that the competitiveness of Chinese tech companies in the AI era no longer relies solely on population scale but on extremely high engineering execution and cost control. This "DeepSeek moment" catalyzed more than interest rate changes themselves, shifting Hong Kong tech stocks from "whipping boys" to "value picks in global tech allocation."

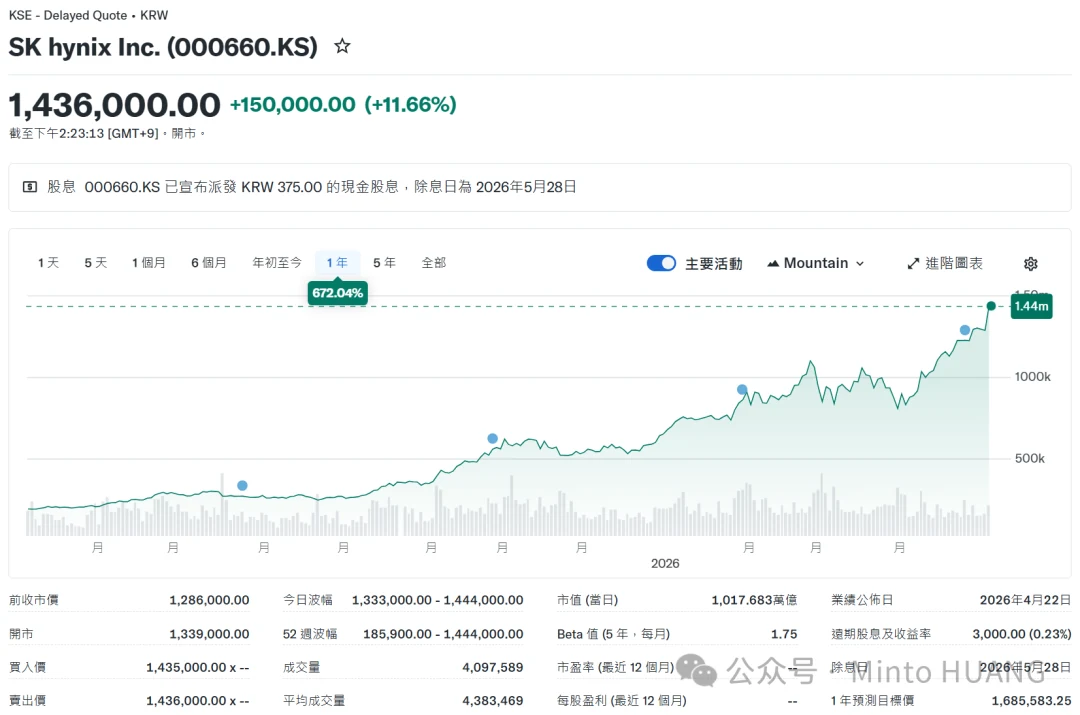

1.2 Global Tech Divergence: The Siphon Effect of Korean Stocks, US Stocks, and the HALO Trade

By 2026, global asset allocation is undergoing a profound "HALO trade"—Heavy Assets and Low Obsolescence. This logic peaked from late 2025 to early 2026.

-

Korea's violent rally and memory chip hegemony: In 2025, the KOSPI far outperformed Hang Seng Tech, driven by Samsung and SK Hynix's monopolistic strength in memory chips (especially HBM4 and DDR5). As global AI data centers shift from compute () to memory capacity, Korean stocks became the biggest beneficiaries of the AI hardware wave, absorbing growth capital that would have gone to Hong Kong tech.

-

US software stocks' crash and hardware pricing power: In stark contrast, US software stocks underwent a brutal valuation correction in 2026. The market found that when hardware costs remain high, SaaS and application-layer profits are being eroded by upstream hardware vendors (Nvidia, memory makers).

-

HALO trade's squeeze on Hong Kong: The global consensus of "heavy hardware, light applications" left Hang Seng Tech's software and platform stocks in an awkward vacuum. Capital preferred chasing expensive hardware stocks over platform stocks with compressed margins.

1.3 Internal Wounds of Core Constituents: The 2025 Financial "Bloodbath"

Looking at the balance sheets of big tech in 2026, the scars from the 2025 "food delivery war" and "AI race" are evident.

-

Meituan: The 2025 performance "abyss." According to Meituan's 2025 earnings preview, due to saturation attacks from JD.com and Alibaba and continued penetration from Douyin's group buying, Meituan's annual net profit saw its largest drop in three years, even recording a massive operating loss in Q3. To defend its delivery market share, Meituan not only "bled" on subsidies but also invested heavily in R&D for frontier areas like drone delivery. This "asset-heavy" transformation led to its stock price grinding at lows in early 2026.

-

Alibaba: Cash flow "bleeding and spin-offs." Alibaba's situation is equally tough. Although its local consumer services segment narrowed losses in 2025, that was based on heavy cash extraction from its retail and cloud businesses. The sustained pressure from the food delivery war caused a significant decline in Alibaba's free cash flow (FCF) in 2025.

-

Xiaomi: Consumer electronics market's "ice and fire." In 2026, Xiaomi's stock has shown extreme volatility. On one hand, its electric vehicles (SU7/YU7) have gained traction; on the other, the sharp rise in memory chip prices in H2 2025 severely compressed its smartphone gross margins. With the global consumer electronics market weakening due to upstream component price hikes, investors' biggest concern is how Xiaomi balances investment in its auto business with defending its traditional business.

1.4 ByteDance: The Lingering "Shadow" Over Hang Seng Tech

As long as ByteDance remains unlisted, the valuation ceiling for Hang Seng Tech will be suppressed.

In 2026, ByteDance's dominance in AI video generation and social commerce has left Tencent and Alibaba gasping. Since ByteDance doesn't need to disclose its loss-making subsidies to capture AI entry points in public markets, this "cost-no-object dimensionality reduction strike" forces Hong Kong-listed companies to face "market share erosion" in every quarterly report. ByteDance is not just a competitor; it's a "pump" draining on-exchange capital to the off-exchange world.

1.5 Valuation Regression: From "Growth Premium" to "Survival Premium"

In the past, we gave Tencent a PE above 30x because it represented the absolute future of social and gaming; we gave Meituan a PE above 30x because it was the ultimate monopoly on lifestyle.

By 2026, these numbers have changed dramatically:

-

Tencent's current PE: ~19x. The market believes its social base is solid, but its identity as a gaming company now outweighs its tech growth attributes.

-

Meituan's current PE: ~12x, PE TTM negative. The market worries whether its asset-heavy delivery model can work in the AI era and whether rising labor costs (rider social insurance, etc.) will permanently lock its profits in single digits.

The core reason for such low valuations is that the "relativity of moats" has been broken. When AI investment in the tens of billions becomes the entry ticket, original channel advantages and user stickiness are being challenged by the "intelligence emergence" of large models.

1.6 Identity Crisis: Are Internet Giants "Infrastructure" or "High-Tech"?

A prevailing view is that the internet has become social infrastructure, like water and electricity. But I think this view is too absolute and even carries a pessimistic misunderstanding.

Whether these internet giants can survive the AI fight depends on whether they can evolve from "platforms" to "sources of intelligence."

-

If they fail to produce leading AI models: They will be relegated to "traditional modern services," enjoying no tech premium and even facing the risk of their preferential 15% tax rate reverting to the standard 25%.

-

If they can build a genuine Generative AI ecosystem: Only then will they qualify as true "high-tech enterprises."

Thus, the Hang Seng Tech Index in 2026 is undergoing a brutal screening based on "AI content." Companies that only collect rent through traditional logic are being abandoned like sunset industries, while those that can truly integrate DeepSeek logic into their proprietary models will be the core targets for the next three years.

2026 Internet War Resumes: From Food Delivery "Brawls" to AI Battles

2.1 Food Delivery Three Kingdoms: Meituan, Alibaba, and JD.com's Zero-Sum Bloodbath

If you looked at Meituan's 2025 earnings, you'd see a thrilling "defense story." By 2026, this war over "stomachs" has become a three-way standoff.

- Meituan: Moat pain and repair

The company expects to swing from profit to loss in 2025, with a net loss of approximately RMB 23.3-24.3 billion, compared to a net profit of about RMB 35.808 billion in 2024—a swing of nearly RMB 60 billion.

The core reason for this "sudden brake" is the collapse of profits in its most profitable segment, "core local commerce": operating profit of about RMB 52.415 billion in 2024 is expected to turn into an operating loss of about RMB 6.8-7.0 billion in 2025. The company emphasizes that this is the result of strategic investment in the ecosystem amid "unprecedentedly fierce competition."

To counter the cross-sector attacks from Alibaba and JD.com in 2025, Meituan was forced to spend tens of billions on subsidies. In 2026, Meituan's strategy has shifted from "full counterattack" to "AI cost reduction." By deploying drones and autonomous delivery robots at scale, Meituan aims to lower per-order delivery costs to below RMB 3, offsetting profit erosion from subsidies. Meituan is not only engaged in defensive subsidies of RMB 5-8 per order but also making a huge bet on R&D. Nearly 35% of that loss was used to accelerate the rollout of autonomous delivery networks (drones and L4 autonomous delivery vehicles). Meituan knows that if it cannot replace human labor with machines to reduce per-order delivery costs before 2026, its original moat will be completely filled in by successive rounds of capital battles.

- Alibaba (Ele.me - Taobao Flash Delivery): Ecosystem synergy reaches critical mass

Alibaba completed a key evolution in 2026: fully integrating Ele.me into Taobao's "instant retail" landscape. The competition is no longer about "delivering food" but "delivering everything." Alibaba leverages its powerful e-commerce supply chain to try to overtake Meituan in the "flash delivery" space.

- JD.com: High-quality assault

JD.com's food delivery business has stabilized at about 15% market share in 2026, with its core weapon being the certainty of service from full-time riders. This forces Meituan to improve rider benefits, further compressing industry gross margins.

- Instant retail (flash delivery) stalemate: From 7:3 to 5:5

The "instant retail" (flash delivery) space reached a historic turning point in 2026. At the end of 2024, Meituan Flash Delivery held about 70% market share thanks to first-mover advantage and a strong delivery network, while Alibaba's Ele.me and Tmall Supermarket (Taobao Flash Delivery) had only about 30%. By early 2026, according to the latest industry data, this situation has evolved dramatically, with both sides approaching a 5:5 stalemate.

Behind this change is Alibaba's "saturation strike" strategy. In 2025, Alibaba fully connected Taobao App's underlying traffic with Cainiao's instant logistics, achieving "everything delivered in 30 minutes." When users realized Taobao could not only sell nationwide but also deliver from nearby, Alibaba's e-commerce mindset successfully transferred to instant retail. Meituan's advantage is no longer unique; instant retail has gone from "one dominant player" to "two giants battling," directly leading to a restructuring of Meituan's valuation logic—it is no longer the unshakeable monopolist.

This competition's impact on valuation is devastating. Meituan's single-quarter loss in Q3 2025 made the market realize how fragile its so-called "monopoly position" is in the face of sustained capital saturation attacks.

2.2 Competing for the Future Traffic Gateway: The "Digital Throat" in the AI Era

The primitive description of "grabbing territory" is no longer sufficient for 2026 competition. The giants are truly competing for the "future traffic gateway landscape." In an era where AI agents are about to take over human digital lives, whoever controls the gateway controls the power to define business rules.

2.2.1 Social Networking and Content Consumption: Tencent and ByteDance's "Dual Rule"

The future traffic gateway landscape is clearly divided into two core camps: "social networking gateway" and "content/interest gateway."

-

Tencent (WeChat): The OS of digital life. WeChat represents the ultimate form of social networking. In 2026, WeChat is no longer just an app but a digital environment embedded with the "Yuanbao" AI assistant. Because social networking carries the highest dimension of trust, WeChat remains the preferred gateway for users to handle "complex affairs"—such as financial transfers, deep communication, and family coordination. Tencent's advantage lies in its "monopoly on private domains," a gateway with strong exclusivity and the most fertile ground for AI to precisely understand individual needs.

-

ByteDance (Douyin): Immersive interest gateway. ByteDance rules users' "aimless time." Through short videos and live streaming, ByteDance has built a "perception gateway" based on real-time algorithmic feedback. By 2026, Douyin has evolved into the world's largest real-time search engine. When you want to learn something, find inspiration, or kill time, Douyin is the first choice. ByteDance's advantage lies in its "violent distribution in public domains," determining what becomes a traffic hotspot.

The truth about future traffic gateways: User behavior is split between "transaction processing (WeChat)" and "interest and social orientation (Douyin)." These two companies lock in over 85% of users' effective mobile time, forming the "twin stars" of future traffic.

2.2.2 Alibaba's Positioning: From "Transaction Platform" to "AI Business Decision Assistant"

Under this dual rule, Alibaba's positioning has undergone a profound shift. It no longer tries to challenge Tencent and ByteDance in social or short-video domains but instead chooses to deepen its "transaction command gateway."

Alibaba's future positioning: The world's most professional AI business decision assistant. If Tencent is the "butler of relationships" and ByteDance is the "window of content," then Alibaba aims to become the "brain for assets and consumption."

-

Logical evolution: Alibaba realizes that users no longer need to flip through pages on Taobao to search; they need AI to tell them: "Which product suits me best?" or "How can I furnish my entire home at the lowest price?"

-

Business moat: Alibaba holds the most complete commercial credit data, supply chain data, and payment闭环 from the past two decades in China. In the AI era, this cold data is the most precious nutrient for training "shopping assistant AI." Alibaba is transforming its Tongyi Qianwen model into a "business operating system." When you initiate a transaction anywhere, the decision support behind it likely comes from Alibaba.

2.3 Valuation Logic's Growing Pains: When the Gateway Shifts from "App" to "API"

This restructuring of traffic gateways has put enormous valuation pressure on the Hang Seng Tech Index.

In the past, internet company valuations were based on app downloads and active users (DAU/MAU). But the 2026 market believes that "apps are dying." When AI agents can call services across apps, platforms that once collected rent at the gateway (like Meituan, JD.com) face the risk of being "de-platformed."

-

Why such low valuations? Taking Meituan as an example, the market worries it will become just a "logistics plug-in" in the future. If users order directly through WeChat's AI or Douyin's AI, Meituan's brand value will be diluted, reducing it to a low-level labor supplier.

-

The suspense of high-tech enterprise certification: This is exactly the point I made earlier: if these big tech companies cannot fight their way out in the AI competition and establish their own "intelligent gateway," they cannot maintain the "tech stock" narrative and will eventually be redefined by capital markets as "asset-heavy delivery companies" or "logistics outsourcers."

From "Bleeding" to "Blood-Making" — Value Restoration and Capital Return Opportunities for Hang Seng Tech

If 2025 was a painful struggle under the dual pressures of "risk premium" and "narrative vacuum," then 2026's main theme is finding certainty. The market is tired of ethereal computing power races and is now scrutinizing the return on investment (ROI) behind every dollar spent. Since its October 2025 peak, Hang Seng Tech has retraced 20%, with a technical breakdown and a 10.1% plunge in February. The core reason for this "worst performance" is not simply fundamental deterioration but the equity risk premium (sentiment and narrative) dragging it down by 14.7 ppt.

3.1 AI's "Coming of Age": From Cost Center to Revenue Center

In the past two years, big tech's AI logic was seen as a "money-burning black hole." But by 2026, market patience with AI has reached its limit. Investors need to see AI spending no longer just as a P&L expense but generating real revenue.

-

AI monetization's "first tier": Tencent's deeply integrated precision advertising system via "Yuanbao" achieved double-digit growth in eCPM by end-2025; Alibaba's Tongyi Qianwen, through its Alibaba Cloud MaaS platform, has locked tens of thousands of SMEs into monthly subscription fees; Meituan's unmanned delivery network began scaled operations in core first-tier cities in early 2026, with per-order cost savings directly converting to operating profit.

-

Narrative logic's "truth-seeking": This shift from "cost" to "blood-making" is the core driver for reversing the Hang Seng Tech Index's performance. Although current dynamic EPS changes still contribute positively to index returns, the market values the migration of "earnings quality" more. When AI can solve corporate survival costs (like Meituan's fulfillment costs) or improve monetization efficiency (like Alibaba's shopping assistant AI), internet companies can truly shed their awkward "asset-heavy service" label.

3.2 Capital Return's "Three Arrows": When Will It Come Back into Focus?

For Hang Seng Tech to stop underperforming A-shares and Nasdaq, three core catalysts need to resonate:

1. Fed Easing Expectations Heat Up: The "Long-Focus Effect" of Liquidity

Although the change in Fed chairmanship in early 2026 (with market fears of a hawkish stance) caused volatility, overall, narrowing interest rate differentials and a weaker dollar theoretically favor Chinese assets.

- Logical anchor: Rate cuts do not automatically drive capital back; fundamentals are the underlying logic. Only when rate cuts are combined with a domestic credit cycle repair will capital return to rate-sensitive markets like Hong Kong.

2. Hong Kong's Unique Structure Returns to Focus: Scarcity at Low Valuations

Hong Kong's unique sectors still offer scarce allocation value for southbound capital.

- Structural advantage: Hong Kong tech is dominated by internet and AI models, contrasting sharply with A-share tech, which is hardware-heavy. After the "China DeepSeek moment" made foreign investors realize the extreme efficiency of Chinese tech in model training costs, internet giants, as leaders in the AI narrative, will regain allocation value. If active foreign capital returns to a neutral weighting in Chinese stocks, it could bring in HKD 500-550 billion in inflows.

3. A-Share Weakness Drives Southbound Inflows: The "Seesaw" Effect

The pace of southbound inflows is influenced by the "seesaw" effect between A-shares and Hong Kong stocks.

- Southbound "pricing power": In 2025, southbound inflows reached about HKD 1.4 trillion, far exceeding 2024's HKD 807.9 billion, with ETFs contributing about HKD 300 billion. Even if maintaining this support in 2026 is challenging, during A-share sector rotations, Hong Kong's unique sectors like dividends, tech, and new consumption remain key structures attracting sustained domestic allocation.

3.3 The "Game Pattern" of Fund Flows: Credit Cycle and Supply Pressure

Against the backdrop of a slowing credit cycle in 2026, the "headwind" from fund flows cannot be ignored.

-

Credit cycle sets the range: In 2026, China's credit cycle may shift from bottoming out in 2025 to oscillating or even slowing down, determining the overall index's elasticity. Estimates show Hong Kong's earnings growth in 2026 is about 3-4%, weaker than A-shares' 4-5%.

-

Threshold for foreign capital return: Long-only Western funds are slow to act and remain significantly underweight. Although active foreign capital flowed into China for seven consecutive weeks in early 2026 (the first time since February 2023), sustainability depends on fundamentals and industry trends.

-

Supply-side pressure: In 2026, Hong Kong's IPO and refinancing demand is about HKD 1.1 trillion, far exceeding 2025's HKD 600 billion. Additionally, the HKD 1.8 trillion lock-up expiration from 2025's large IPOs could become a potential pressure.

The Tax "Sword of Damocles" — Loss of High-Tech Status and Systematic Revaluation of Financial Models

If the 2025 competition losses were "surface wounds," then the 2026 rumors about "internet giants losing their high-tech enterprise status" are a direct hit to the industry's lifeline.

4.1 Structural Shift in Fiscal Pressure: From "Land" to "Profits"

Combining the latest fiscal data from late 2025 to early 2026, we can clearly observe a dramatic change in local fiscal logic. With the long-term adjustment of the real estate cycle, land sales as a share of local fiscal revenue have fallen to historic lows. To maintain social security, hard-tech R&D (semiconductors, quantum computing), and new infrastructure spending, the fiscal system must find new, stable, high-margin tax bases.

In this context, internet giants with annual profits in the tens or even hundreds of billions naturally enter the core of tax scrutiny. Over the past decade, under labels like "software development" and "modern services," these giants have enjoyed a 15% preferential tax rate for high-tech enterprises. But in the 2026 regulatory context, a soul-searching question emerges: Is a platform that profits from food delivery commissions, live-streaming e-commerce, and social ads truly equivalent to "hard tech"?

4.2 Financial Calculation: The "Earnings Kill" from a 10% Tax Rate Difference

Let's conduct an extreme stress test based on expected 2026 financials. Assume regulators tighten the criteria for "high-tech enterprise" certification—requiring core underlying patents, hardware R&D exceeding 30% of revenue, and excluding pure commercial matchmaking businesses.

-

Tencent: Tencent's profit core is social ads and gaming. If its effective tax rate rises from 15% to the standard 25%, its net profit attributable to shareholders would shrink by about 12%. This would instantly lift its P/E ratio at the same stock price, triggering passive selling.

-

Meituan: Meituan's situation is more awkward. Its food delivery business is already low-margin, heavily reliant on scale effects and tax breaks. Once the preferential treatment is lost, its just-repaired unit economics would turn negative again, adding insult to injury for its stock price, which is trying to bottom out.

-

Alibaba: Alibaba is desperately trying to tax-isolate "Alibaba Cloud" from "Taobao and Tmall Group." Alibaba's narrative is that its cloud business is hard tech (15% tax), while its e-commerce business should be classified as general retail (25% tax). This "identity split" will be the main theme of tax planning for big tech in the next three years.

4.3 Local Government's Game: Support or Harvest?

In 2026, local governments' attitudes toward big tech have become nuanced. Beijing, Hangzhou, and Shenzhen, as headquarters locations, need the jobs and ecosystems these giants bring, but they also face central government assessments of "fiscal revenue quality." Rumors of a "3% tax rate increase for the three major telecom operators" are actually a signal: excess profits in basic public service industries must be returned to society through taxation. The positioning of internet companies in 2026—will they shift from "protected infants" to "tax pillars"? This identity change directly locks in the valuation ceiling for the internet sector—you can't have both the stability of public utilities and the high premium of tech stocks.

AI Narrative's "Three Kingdoms" — Who's Swimming Naked, Who's Evolving?

After the 2026 red envelope wars, the market has entered the "post-traffic era." Simple DAU growth no longer impresses investors; they care more about AI's "chemical reaction" with existing businesses.

5.1 ByteDance: The Violent Extension of Algorithmic Hegemony

ByteDance's AI narrative is the most terrifying to its peers. Its logic is not "AI + business" but "AI is business."

-

Core advantage: ByteDance has the world's most real-time, highest-frequency user feedback data. Doubao's success in 2026 is essentially the rebirth of Douyin's algorithm in a dialog interface.

-

Source of valuation discount: As long as ByteDance remains unlisted, it acts like a black hole, sucking away all "growth expectations" from Hong Kong tech stocks. Investors will think Alibaba's AI is just doing addition, while ByteDance's AI is doing multiplication.

5.2 Alibaba: Computing Power Foundation and "AI Industrialization"

Alibaba's narrative logic has the style of an "old hegemon": not fighting for one city or one pool, but for the foundation of the world.

-

MaaS (Model as a Service): Tongyi Qianwen has become the preferred choice for domestic SMEs to deploy AI in 2026. Alibaba's logic is that even if its own apps don't capture traffic, as long as you run AI on its cloud, it makes money.

-

Challenge: This asset-heavy model faces huge depreciation pressure in the high-interest-rate environment of 2026 (even with Fed rate cuts, computing costs remain high). When Alibaba Cloud can shift from "revenue growth" to "profit explosion" is key to whether Alibaba's stock can return to HKD 180.

5.3 Tencent: The Ultimate "Lubricant" of the Connector

Tencent's AI narrative is the most introverted and the most lethal.

-

Hunyuan Large Model: Tencent Yuanbao doesn't emphasize "omniscience" but "omnipresence." In 2026, Yuanbao is deeply embedded in the WeChat ecosystem, helping you write weekly reports, book restaurants, and manage finances. Tencent's logic: I don't change your behavior; I just make every second you spend on WeChat more efficient.

-

Valuation anchor: Tencent's AI narrative is to protect its 25% high-margin advertising business. As long as AI can improve ad matching rates, Tencent is unbeatable.

Valuation Restructuring After Paradigm Shift and the 2026 Full-Year Verdict

Looking back at 2026, it's not just the Year of the Horse Spring Festival red envelope frenzy but the most profound "demythologization movement" in Chinese internet history. The weakness of the Hang Seng Tech Index is essentially the result of the共振 of blocked macro liquidity, a slowing credit cycle, and zero-sum industry competition. When the traditional "scale growth" narrative fails, investors must establish a new valuation model based on "efficiency" and "certainty."

6.1 Valuation Modeling Suggestions for the Next Three Years: Internet Is No Longer Purely "Tech Stocks"

In the 2026 fiscal environment, big tech faces a role shift from "high-tech darlings" to "tax mainstays." When building financial models, investors should incorporate the following modified variables:

-

Evolution of Sum-of-the-Parts (SOTP) valuation: Mature businesses (foundation): Tencent's social ads, Alibaba's core e-commerce, Meituan's in-store services should be conservatively priced at 8-10x P/E, treating them as "utilities" that provide cash flow.

-

AI business (option): For AI models with profitability (like Mingle or Tongyi B-end subscriptions), they should be priced separately using P/S or risk-adjusted DCF. You'll find that many giants' current stock prices only account for mature businesses, with AI's "blood-making" ability almost given away for free by the market.

-

DCF model's "fiscal correction": Tax rate reversion assumption: The effective income tax rate must be assumed to gradually rise from the 15% preferential rate to the 25% standard rate as a medium-to-long-term baseline.

-

Capital expenditure (Capex) normalization: 12-15% of revenue must be locked in as rigid R&D spending on AI computing power and algorithms to maintain competitiveness after the "DeepSeek moment."

6.2 2026 Full-Year Summary: The "Quality Test" Under Identity Reversion

China's internet in 2026 is at the painful endpoint of returning from "dream P/E" to "earnings P/E" and even "book P/E."

-

Index structural divergence: The Hang Seng Tech Index's "worst performance" is primarily due to risk appetite (equity risk premium) dragging it down by 14.7 ppt, not a complete earnings collapse. The top 5 weight stocks contributed 6.0 ppt of the decline, indicating the market is brutally repricing the "old kings."

-

Tight fund flow balance: Looking ahead to 2026, Hong Kong's fund flow environment may not surpass 2025, with a supply scale of HKD 1.1 trillion (IPOs and refinancing) similar to demand. This means the market will be extremely structured, and allocation must closely follow the direction of "credit expansion."

-

Narrative logic shift: The quality of internet giants no longer depends on how many red envelopes they give out but on the divergence between "leaders and laggards" in the AI narrative. Only those that can truly use AI to reduce fulfillment costs (like Meituan) or improve monetization efficiency (like Tencent) deserve the title of "core assets."

💡 Conclusion: Deep Roots Survive

The internet after 2026 is no longer an era of "fast fish eating slow fish" but an introverted era of "deep roots survive." Traffic dividends will peak, tax breaks will fade, and the Fed's rate cut expectations may also face variables due to the new chair's hawkish stance.

But as the HKD 300 billion net inflow into ETFs by southbound capital in 2025 revealed, Hong Kong-listed targets with the dual attributes of "high dividend + AI option" remain the anchor for domestic and long-term foreign capital in turbulent times. At the end of this long analysis, the conclusion is clear: Abandon the illusion of "explosive growth" and embrace the premium of "efficiency." Companies that can maintain free cash flow growth despite high CapEx will be the true protagonists returning to center stage in the next three years.

Risk Disclaimer: The views in this article are for reference only and do not represent any investment advice. Markets are risky; invest with caution.

专注投资分析、市场洞察与资产配置。不追短期波动,只理解真正驱动长期回报的东西。