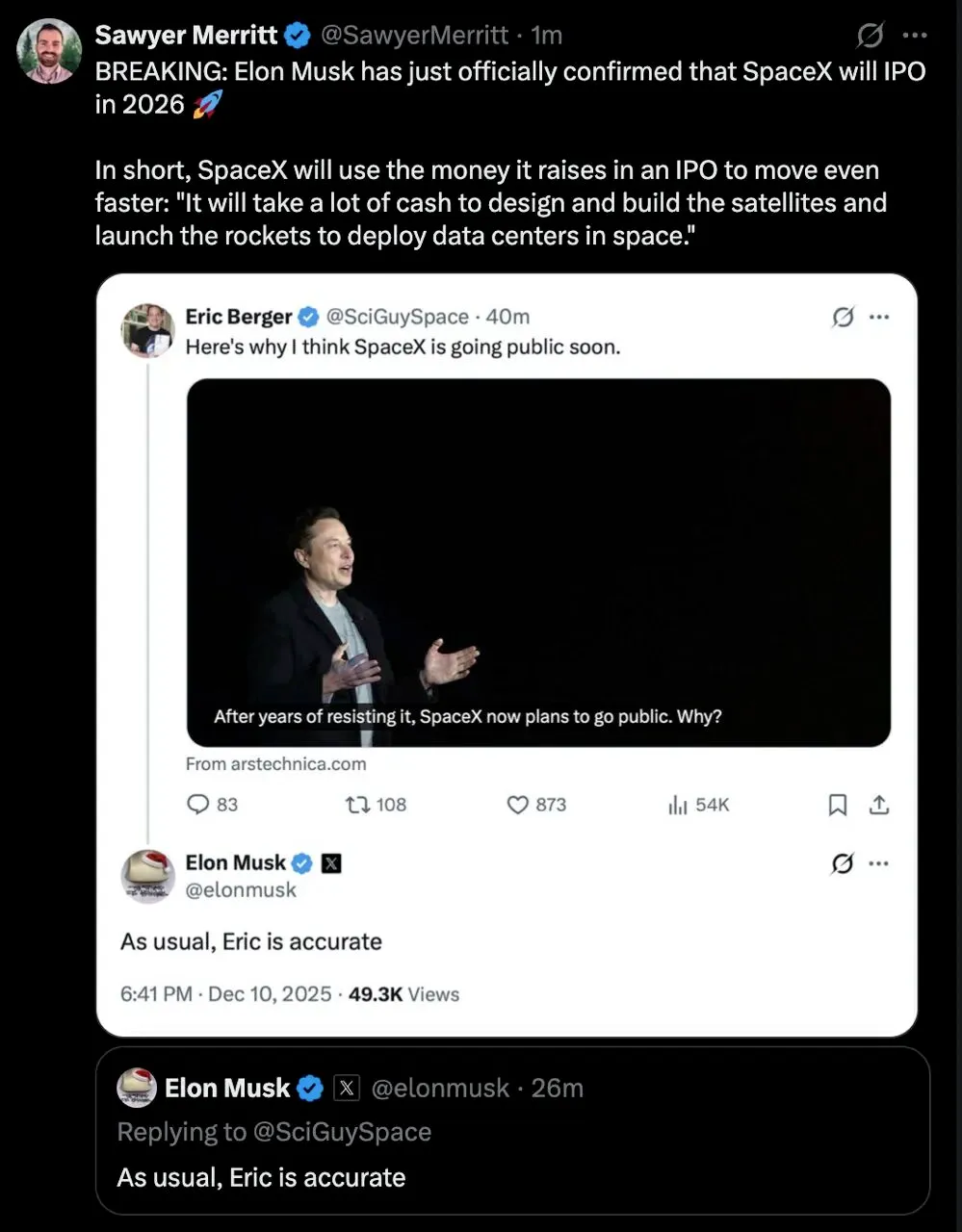

As I started writing this, Musk just confirmed SpaceX's imminent IPO. The space sector is hot—RKLB, ASTS, and others have rebounded strongly. I believe space-related supply chain companies will be a hot investment theme in 2026. As the industry leader, studying SpaceX is urgent.

So let's start from a third-party perspective and decode ARK Invest's report titled "ARK's Expected Value For SpaceX In 2030: ~$2.5 Trillion Enterprise Value."

The latest joint report from ARK Invest and Mach33 gives SpaceX a stunning valuation anchor: by 2030, the company's expected enterprise value will reach $2.5 trillion. That implies a CAGR of 38% from its last funding round in December 2024 at $350 billion. This valuation model isn't built on launch services alone, but on a self-reinforcing flywheel: 's cash flow fuels Starship's rapid iteration, which in turn dramatically lowers launch costs via Wright's Law, ultimately funding the book value of Mars colonization infrastructure. This article will dissect the three core variables behind this model: bandwidth economics, launch cost curves, and the accounting revaluation of Martian assets.

The report drops a bombshell right away: ARK divides SpaceX's valuation into three scenarios—base case $2.5 trillion, bear case $1.7 trillion, and bull case $3.1 trillion. According to the joint research model by ARK Invest and Mach33, by 2030, SpaceX's enterprise value is expected to reach $2.5 trillion. That means a CAGR of 38% from its roughly $350 billion valuation in December 2024.

For rigorous investors, such a massive valuation increase can't rest on grand narratives alone. We need to strip away market sentiment and dig into the model's core to find the financial pillars supporting a trillion-dollar market cap.

Chapter 1: Valuation Panorama: Probability Distribution Under Monte Carlo Simulation

When we talk about $2.5 trillion, we must first clarify: in financial engineering, it's not a deterministic prediction but the expected value of a probability distribution. ARK's team built a dynamic model with 17 independent variables (including satellite lifespan, launch costs, end-user pricing, etc.) and ran one million simulations to map out SpaceX's future value probability cloud.

These three typical scenarios form the coordinate system for understanding SpaceX's investment returns:

1.1 Base Case: The $2.5 Trillion Expected Anchor

This is the model's core output, closest to the statistical expectation. In this scenario, SpaceX's enterprise value in 2030 reaches $2.5 trillion. This valuation implies a dual pricing logic: the market sees SpaceX not only as a monopolist in global communications infrastructure (like a telecom operator) but also as the sole provider of interplanetary transport (like the East India Company in the Age of Sail).

1.2 Bull Case: $3.1 Trillion Nonlinear Explosion

If we assign higher weight to SpaceX's execution or assume global broadband demand is more elastic than expected, the model enters the 75th percentile bull case. Here, the valuation could exceed $3.1 trillion. This typically corresponds to breakthrough progress in Starship reusability or an explosive penetration of Starlink in developing countries. In other words, there's a 25% chance that its market cap surpasses the world's most valuable tech giant today.

1.3 Bear Case: $1.7 Trillion Margin of Safety

Even in the most conservative 25th percentile simulation, SpaceX's valuation still reaches $1.7 trillion. This reveals a high margin of safety—even with regulatory headwinds, launch failures, or slowing user growth, as long as the business loop doesn't collapse systemically, its value floor is several times its 2024 funding valuation (~$350 billion) and nearly double the $800 billion valuation given this year.

Chapter 2: The Physics of the Business Model: The Capital Flywheel from Earth to Mars

To deconstruct SpaceX's internal workings, we can't simply apply traditional manufacturing's "cost-plus" or internet companies' "traffic monetization" logic. ARK's model reveals a unique, self-reinforcing "physics flywheel" that tightly couples cash flow, physical payload, and interplanetary vision into a cross-planetary capital cycle.

2.1 Flywheel Ignition: Earth-Based Cash Pump

The flywheel starts in Earth orbit. Initially, SpaceX uses financing cash to build rockets and satellites. This looks like massive CapEx, but it's actually building core assets. As Falcon 9 puts satellites into orbit, these physical assets quickly become "orbital bandwidth" capacity. Once bandwidth is formed, SpaceX sells high-speed internet services to global users as a "digital good." As Starlink's subscriber base grows exponentially, the resulting free cash flow isn't used for dividends or buybacks but is immediately reinvested: part goes to more satellites to expand the network effect, and the rest flows to longer-term R&D—Starship and Mars colonization technology.

2.2 Flywheel Acceleration: The Constellation Completion Tipping Point

This cycle has a critical phase transition. The model assumes Starlink's full constellation completion around 2035. Before that, the system is in a "blood transfusion" phase—every dollar of revenue is used to expand coverage. Once the constellation is complete, CapEx drops sharply, requiring only routine replacement. At that point, massive free cash flow is unleashed. The flywheel's center of gravity shifts strategically: from Earth orbit "commercial monetization" to deep space "infrastructure building."

2.3 Flywheel Endgame: Assetization of Mars Colonization

This is the model's most disruptive perspective. In traditional financial statements, Mars plans are pure expense or sunk cost. But in ARK's model, Mars is reframed as an expansion of the balance sheet. Once Earth-based cash flow covers operating costs, the remaining massive funds are used to build Starship fleets, develop Optimus robots, and send them to Mars. Each launch and each robot landing on Mars becomes "book value" on SpaceX's balance sheet. This cross-planetary capital allocation model—"earn on Earth, save on Mars"—is the irreproducible premium behind its $2.5 trillion valuation.

Bear case:

Base case:

Bull case:

Chapter 3: Starlink Economics: The Micro-Foundation of Trillion-Dollar Revenue

In the flywheel model, Starlink is the undisputed cash cow. To support a trillion-dollar valuation, Starlink must show dominant unit economics. ARK's model reveals the mathematical foundation of its profitability through a "top-down bandwidth supply-demand analysis."

3.1 Physical Limits and Economic Efficiency of Bandwidth

First, look at the supply side's core metric—total system bandwidth. According to the Monte Carlo simulation average, SpaceX's global total bandwidth capacity is expected to peak at around 130 million Gbps (130 Pbps). This physical boundary defines its user ceiling. But more critical than the total is the "breakeven point." The model estimates that Starlink needs only about $0.20 per Mbps per month in revenue to cover its operating and depreciation costs. This number is devastatingly low. The average US broadband unit price is far higher. At $0.20, the cost line is about 75% below the industry average. This gives SpaceX incredible pricing power: in developed markets, it can charge high prices for excess profits; in price-sensitive Global South markets, it can drop prices to levels traditional operators can't match while still generating positive cash flow.

3.2 The $300 Billion Annual Revenue Blueprint

Based on these unit economics, the model makes a bold long-term revenue projection: by around 2035, when the constellation is fully mature, SpaceX's annual revenue could reach about $300 billion. To put that in perspective, that's about 15% of global telecom service spending at that time. In other words, for every $7 spent on global communications, more than $1 flows to SpaceX. This penetration of the physical layer of global information infrastructure provides endless funding for its Mars journey.

3.3 Moore's Law for Satellites (Wright's Law)

Starlink's ability to maintain low costs and high bandwidth relies on continuous satellite technology iteration. The model notes that Starlink satellite performance improvement follows Wright's Law: each doubling of cumulative production reduces unit cost by a fixed percentage. From V1 to V2 Mini to the planned V3, each iteration is an exponential leap in performance. SpaceX has planned next-generation satellites with masses up to 2,000 or even 4,000 kg, targeting 1 Tbps per satellite. This explosion in per-satellite performance allows SpaceX to deliver more network capacity (revenue) with fewer satellites (lower CapEx).

Chapter 4: The Starship Revolution: Reshaping the Cost Curve of Space Transport

If Starlink solves "what to sell," Starship solves "how to deliver." In ARK's valuation model, Starship is not just a heavy-lift rocket; it's the key variable rewriting the cost equation of the aerospace industry.

4.1 Wright's Law Verified at the Launch Pad

The aerospace industry has long suffered from high launch costs, but SpaceX is breaking the curse. Based on Falcon 9 historical data, the model finds that each doubling of cumulative mass to orbit reduces rocket turnaround time by a constant 27%. This efficiency improvement curve strikingly matches Wright's Law. Shorter turnaround means higher reuse frequency. As Starship matures, the fixed cost per launch is diluted by massive launch cadence, with marginal cost approaching fuel cost.

4.2 Fundamental Inversion of Cost Structure

With extreme full reusability, the cost structure of space launches will undergo a quiet revolution. The model predicts that in early stages, launch costs dominate total mission cost. But by the late 2030s, this ratio will invert: satellite manufacturing costs will account for about 90% of total cost, while launch costs drop to a negligible 10%. This is a highly strategic insight. It means SpaceX is turning expensive "space transportation" into cheap "space logistics." When transport cost is no longer a bottleneck, SpaceX gains enormous freedom in satellite design—it can build larger, heavier, more capable satellites without spending millions on weight-saving measures. This "capacity overabundance" creates a moat competitors can't cross.

Chapter 5: Martian Assets: From Sci-Fi Dream to Balance Sheet

In traditional financial analysis, Mars exploration is often seen as a founder's hobby. But ARK's model offers a forward-looking financial perspective: incorporating Mars into a serious valuation framework, defining it as SpaceX's most important new asset class (PPE).

5.1 Interplanetary Assets Defined at Book Value

Since Mars projects won't generate traditional commercial revenue (like trade or tourism) in the near term, the model uses a "replacement cost" approach: the enterprise value of the Mars business equals cumulative cash flow allocated to Mars R&D plus the book value of infrastructure built on Mars. This logic implies a deep judgment: as Starlink matures around 2035, SpaceX becomes a giant cash machine, and Mars is the reservoir for that wealth. Every dollar spent on Mars becomes human civilization's infrastructure on another planet—landing pads, power stations, habitats. These assets, though illiquid, represent SpaceX's monopoly on future interplanetary living space.

5.2 Optimus Robots: Capitalizing Martian Labor

In the composition of Martian assets, Optimus humanoid robots play a crucial role. The model assumes future Mars missions will rely heavily on environment-adapted Optimus robots rather than expensive, fragile human astronauts. Projections show that by 2040, the deployed Optimus robot fleet on Mars could reach millions. These robots are the main workforce for Mars development, tirelessly building infrastructure. As robot productivity increases, the "book value" they create grows exponentially. In the valuation model, these robots have a dual nature: they are both assets themselves and capital goods that create new assets.

5.3 The Unusual Nature of Long-Term Capital Returns

The model also candidly notes that given the grand scale of Mars colonization, investors are unlikely to see direct cash dividends from Mars projects for a long time. Early-stage Mars development is more about asset accumulation than monetization. Yet this long-term, strategic asset accumulation is the indispensable "premium" in the $2.5 trillion valuation. It represents the market's risk pricing of SpaceX as the sole executor of the "multi-planetary species" vision.

Chapter 6: Risks and Variables: Fragility Behind the Model

Despite the thrilling $2.5 trillion vision, a rigorous financial analysis must acknowledge the tail risks in the model.

6.1 Execution Risk: The Technical Challenge of Starship Reuse

A core assumption is that Starship achieves rapid, cheap full reusability. If Starship's thermal protection system or Raptor engine reuse life falls short, extending turnaround time, the entire model's economic foundation will be shaken, and Starlink V3 deployment costs will rise significantly.

6.2 Key Man Risk

SpaceX's innovation culture and execution depend heavily on Elon Musk's personal leadership. The model admits that unforeseen events causing management turmoil could lead to strategic drift, triggering a sharp valuation de-rating.

6.3 Market and Policy Dynamics

Although SpaceX is currently dominant, competitors like Amazon Kuiper could compress the total addressable market for broadband. Additionally, Starshield relies heavily on US defense budgets; geopolitical and government spending fluctuations could impact this high-margin revenue.

Conclusion

When we re-examine that $2.5 trillion number, we see not a simple financial forecast but a grand blueprint for humanity's future. ARK Invest and Mach33, through detailed data and precise modeling, show that SpaceX's high valuation isn't built on a bubble but on solid physics and economics.

From Starlink's trillion-dollar cash flow, to Starship's transport cost revolution, to the strategic accumulation of Martian assets, these three links form an unprecedented business loop. For investors, understanding SpaceX's valuation is understanding the economics of human civilization's expansion. That $2.5 trillion is both a discount of future cash flows and an early bet on humanity's ultimate destiny: leaving Earth's cradle and becoming a multi-planetary species.

专注投资分析、市场洞察与资产配置。不追短期波动,只理解真正驱动长期回报的东西。