Rocket Lab reported its third-quarter financial results after the bell last night. The company posted record total revenue for the quarter, with profitability significantly exceeding market expectations, while delaying the Neutron rocket's arrival at the launch site to Q1 2026 to ensure reliability and performance.

Financial Performance & Growth Analysis

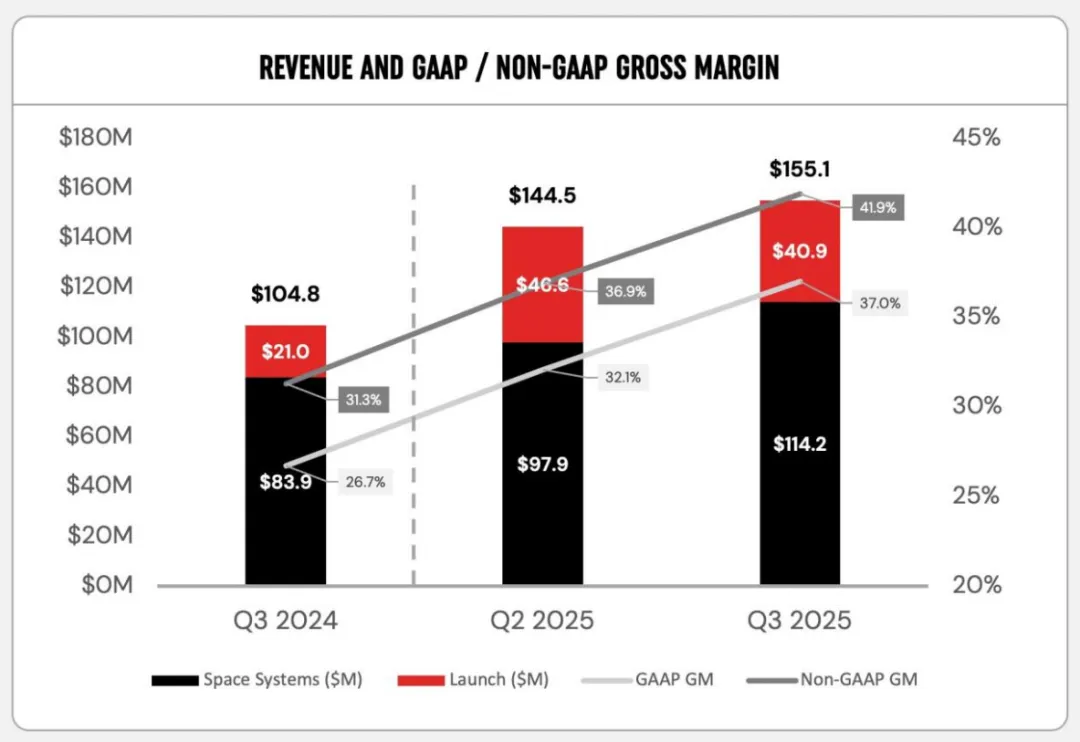

Rocket Lab delivered a strong Q3 2025, with total revenue reaching $155.1 million, up 48% year-over-year. This beat the market consensus of $151.72 million.

Profitability improved dramatically, with a GAAP EPS loss of $0.03, far better than the expected loss of $1.0. Gross margins hit record highs: Non-GAAP gross margin of 41.9% and GAAP gross margin of 37%.

Note that the large EPS beat was partly due to one-time benefits: an accounting adjustment that pulled some HASTE mission profits into the quarter, and a 100% margin launch cancellation fee. Management noted that even excluding these adjustments, Q3 EPS exceeded guidance.

Backlog continued to grow, reaching $1.1 billion at quarter-end (up from $1.0 billion last quarter). Launch Services backlog rose to $509.7 million, up 56% YoY, driven by 17 new dedicated Electron launch contracts signed in the quarter. The company expects about 57% of total backlog to be recognized as revenue over the next 12 months.

Dual Engine Growth: Space Systems & Launch Services

Both core segments delivered significant growth:

- Space Systems: Revenue of $114.2 million, up notably YoY, driven by continued strong performance in satellite manufacturing (QoQ up 16.7%). The Space Development Agency (SDA) declared Rocket Lab's components, systems, and software for 18 T2TL satellites "mission ready," and the company is moving toward full production. With over $1 billion in liquidity, Rocket Lab is pursuing strategic M&A, including the acquisition of GEOST and a planned acquisition of Germany's Mynaric, to expand end-to-end capabilities and optical systems manufacturing. Management noted that contract awards for the SDA Tranche 3 Tracking Layer (about 54 satellites, potentially the largest contract in company history) have been delayed by the U.S. government shutdown.

- Launch Services: Revenue of $40.9 million, up 95% YoY, driven by 4 Electron launches in Q3, versus 3 in the year-ago period.

Neutron Development: Delay Reasons & Current Progress

The timeline for Neutron's first flight hardware to arrive at the launch site has been pushed to Q1 2026. This adjustment reflects the company's philosophy of prioritizing "integrity and performance," requiring all systems to undergo intensive qualification testing and acceptance procedures before the rocket arrives at the pad.

Current Progress & Peak Investment:

- Testing & Engines: The company is conducting extensive testing across the entire launch vehicle, including propulsion systems, thrust structure, and first and second stage tanks. Archimedes engines for the first launch are completing or near completion of testing, currently running 20 hours a day, 7 days a week, with stable performance.

- Infrastructure: Launch Complex 3 (LC3) at Wallops Island, VA, is now officially activated, with final commissioning underway to prepare for flight hardware pre-launch testing.

- R&D Costs: Neutron development spending is at its peak. Due to accelerated development, total R&D costs for Neutron are now expected to reach $360 million, up from the initial estimate of $250-300 million.

Neutron Launch Plan & Profitability Outlook

Neutron's first launch will occur after flight hardware arrives at LC3 in Q1 2026 and successfully completes all vehicle qualification tests and acceptance procedures.

The company has outlined post-first-flight launch cadence:

- Within 12 months of first flight: Plan to execute 3 missions.

- In the following 12 months: Plan to execute 5 or more missions.

Currently, Neutron's backlog includes two dedicated launch missions, with one rideshare mission not yet booked.

On profitability, management expects Neutron's Non-GAAP gross margin to be at least in line with Electron's level (Electron's Non-GAAP gross margin outlook is 45%-50%).

Q4 Outlook: The company expects Q4 revenue to continue growing, in the range of $170 million to $180 million. Non-GAAP gross margin is expected to remain high, between 43% and 45%.

Overall, this was a relatively strong earnings report, but we may need to wait until the next quarter for more details on Neutron's on-pad or launch timeline. I will continue to track Rocket Lab's progress.

Risk Disclosure: The views expressed herein are for informational purposes only and do not represent investment advice. Market risk exists; invest with caution.

专注投资分析、市场洞察与资产配置。不追短期波动,只理解真正驱动长期回报的东西。