The market is entering a new phase. The Fed's rate-cutting policy carries some uncertainty, but what is certain is that the rate-cut cycle is not over, providing potentially favorable financing conditions for the innovative drug track. The innovative drug industry is characterized by high R&D investment, long cycles, and high returns. A low-interest-rate environment helps lower corporate financing costs, enabling sustained R&D spending. At the same time, global aging and rising healthcare demand offer a broad market for innovative drugs. Moreover, increased awareness of disease prevention is accelerating breakthroughs in biomedical technology and policy support, further driving industry innovation. Therefore, driven by policy, capital, and demand, the innovative drug track has long-term growth potential.

Innovative Drug Track

I. Beta of Innovative Drug Sector: Systemic Drivers and Cyclical Fluctuations

(A) Demographic Change as the Underlying Logic

-

Quantitative Impact of Aging and Disease Spectrum Shift

- Global aging is accelerating: According to the UN, the global population aged 65+ will rise from 10% to 16% by 2050. In China, the population aged 60+ will exceed 400 million by 2035 (30% of total), directly boosting demand for drugs in oncology, Alzheimer's, and osteoarthritis.

- Chronic disease economic burden: WHO statistics show chronic diseases account for 70% of global deaths. China's diabetes treatment market alone exceeds RMB 100 billion, but the efficacy gap for complications (e.g., diabetic nephropathy) remains 60%.

- Emerging market middle class rise: Per capita medical spending in India and Southeast Asia grows 8-12% annually, driving penetration of targeted oncology drugs and biosimilars (e.g., PD-1 use in India up 5x in 3 years).

-

Structural Opportunities from Health Awareness Upgrade

- Preventive healthcare demand: The cancer early screening market CAGR is 18% (e.g., Grail's Galleri multi-cancer test covers 50 cancers), driving companion diagnostics and integrated treatment solutions.

- Patient willingness to pay stratification: In China, high-net-worth individuals use innovative drugs out-of-pocket at over 30% (e.g., CAR-T therapy at RMB 1.2 million per course still in short supply), promoting a dual-track system of high-end medical market and universal health insurance.

(B) Policy as the Strongest Cycle in Pharma

-

Global Regulatory Paradigm Shift

- Accelerated review mechanisms: FDA's RTOR (Real-Time Oncology Review) shortened Keytruda's esophageal cancer approval to 4 months; in 2023, 60% of China's conditional approvals were for oncology drugs.

- Payment reform: The US IRA requires price negotiations for top 50 drugs starting 2026, expected to cut pharma revenues by 5-15%; China's医保 negotiations balance cost control and innovation incentives via "simple renewal" rules (23 new innovative drugs added in 2023).

-

Geopolitical Policy Risks and Opportunities

- Supply chain security: The US BIOSECURE Act restricts WuXi AppTec and other CXOs from federal projects, forcing Chinese pharma to accelerate localization of culture media and fillers (import dependence still >80%).

- Regional market games: Middle East "medical tourism" policies attract cell therapy centers (e.g., Saudi Arabia invested $460 million in a gene therapy base); Chinese firms can enter emerging markets via tech licensing.

(C) Industry Black Swan Events: Unpredictable but Powerful

-

Public Health Crises Catalyze Tech Breakthroughs

- Paradigm shift from COVID vaccines: Moderna's mRNA platform valuation surged from $5B (2019) to $180B (2021), validating platform tech's explosive potential.

- Long-term R&D direction reshaped: Post-pandemic, new broad-spectrum antiviral projects increased 300% (e.g., Pfizer's Paxlovid 3CL protease target spawned 15+ pipeline candidates).

-

Tech Black Swan Events: Two-Way Impact

- Gene editing ethics controversy: CRISPR-Cas9 patent disputes caused Editas and Intellia stock swings >40%, highlighting legal risks.

- Cell therapy safety crisis: Bluebird Bio's LentiGlobin clinical hold due to suspected carcinogenic risk triggered reassessment of viral vector integration risks.

(D) Market Risk Appetite Shifts Affect Capital Flows

- Capital Cycle Transmission Mechanism

- Interest rate sensitivity and valuation models: During the Fed rate hike cycle (2022-2023), the Biotech Index (XBI) saw a max drawdown of 55%, as higher WACC in DCF models directly depressed forward pipeline valuations.

- Risk appetite indicators: When VIX >30, biotech ETF net outflows can reach $500M daily, showing risk-off sentiment's dampening effect on the sector.

II. Alpha of Individual Innovative Drug Stocks: Sources of Excess Returns

(A) rNPV Valuation Framework: Room for Arbitrage

-

Expectation Gaps in Success Rate Assumptions

- Bayesian revision by clinical stage: Phase I success rates are typically 10%, but projects with biomarker stratification (e.g., HER2-low breast cancer) can reach 25%. For example, Daiichi Sankyo's DS-8201, due to its unique payload technology, has a clinical success rate 3x higher than traditional ADCs.

- Regulatory communication premium: Drugs with FDA Breakthrough Therapy designation see Phase II-to-approval success rates jump from 7% to 45% (e.g., Blueprint's RET inhibitor Gavreto).

-

Cognitive Gaps in Penetration Rate Estimation

- Treatment paradigm substitution space: Novartis' radioligand therapy Pluvicto reached 40% penetration in late-line prostate cancer; expanding to second-line could add $2B in market.

- Payment innovation unlocking demand: Vertex's CFTR modulator, via a "pay-for-performance" agreement (25% of sales tied to FEV1 improvement), boosted patient usage by 50%.

(B) Clinical Trial Surprise Strategies

-

Art of Clinical Endpoint Design

- Revaluation of surrogate endpoints: Biogen's Aβ antibody Aduhelm was approved based on amyloid plaque clearance, but later withdrawn, sparking debate on surrogate endpoint weighting.

- Cross-trial data application: Merck's Keytruda leveraged IMbrave150's OS data in adjuvant liver cancer, shortening clinical development by 2 years.

-

Event-Driven Arbitrage Opportunities

- Volatility patterns around data readouts: Statistics show that 30 days before major conferences like ASCO, stock volatility of relevant companies rises 40% on average, but only 20% of data truly beats expectations.

- Short-selling strategies: For overvalued companies with obvious clinical flaws (e.g., Theranos-style fraud), firms like Muddy Waters use professional medical due diligence to achieve short gains.

(C) Capturing Inflection Points in Company Growth

-

Network Effects of Platform Technologies

- Moderna's mRNA ecosystem: From COVID vaccine to personalized cancer vaccines (PCV), its platform has spawned 45+ pipeline candidates, with marginal R&D costs down 60%.

- WuXi Biologics' CRDMO model: By "following the molecule" to bind client R&D processes, customer retention rate reaches 95%.

-

Nonlinear Jumps in Commercialization Capability

- Multiplier effect of sales funnel: BeiGene's Brukinsa, through head-to-head trials beating Imbruvica, pushed overseas sales share from 10% to 60%.

- Compounding effect of indication expansion: AbbVie's Humira formed a "patent thicket" with 79 indications, extending its lifecycle by 15 years.

III. Investment Advice: Building a Balanced Portfolio

(A) Beta-Level Allocation Logic

-

Cycle Timing Tools

- Policy cycle tracking: Build quantitative models for drug regulatory review efficiency,医保 negotiation price cuts, etc. For example, China's IND approval time for innovative drugs has shortened from 24 months to 12 months.

- Capital cycle contrarian positioning: When biotech IPO numbers hit 5-year lows and M&A activity heats up (e.g., Q4 2023), it is often a bottom-fishing opportunity.

-

Regional Risk Diversification

- Developed markets: Allocate to Big Pharma with strong cash flows (e.g., J&J, Novartis) to hedge interest rate risk.

- Emerging markets: Focus on Chinese Biotech with strong license-out capabilities (e.g., BeiGene, RemeGen) to share global innovation dividends.

(B) Alpha-Level Selection Strategy

-

Tech Moat Identification Framework

- Patent quality assessment: Calculate patent cliff curves (e.g., Keytruda's sales may drop 70% after patent expiry in 2028); prefer platform-type patent companies.

- Clinical data moat: Focus on drugs with OS significantly superior to standard of care (e.g., AstraZeneca's Tagrisso with median OS of 38.6 months in lung cancer).

-

Management Team Quantitative Assessment

- Founder background premium: Statistics show that Biotech IPOs led by serial entrepreneurs deliver 25% higher 3-year returns than industry average.

- R&D efficiency metric: Measured by "number of clinical-stage pipeline candidates per $100M R&D spend," Regeneron leads at 1.2 candidates/$100M.

IV. Risk Analysis: Multi-Dimensional Dynamic Monitoring

(A) Policy Risk Prediction Models

- 医保 Negotiation Price Prediction Algorithm

- Based on pharmacoeconomic evaluation (QALY cost threshold typically $50K/year) and competitive landscape (e.g., PD-1 entering "5-to-3" knockout), build price cut prediction models with error margin within ±15%.

(B) Clinical Risk Hedging Tools

- Negative Correlation Design in Pipeline Portfolio

- Allocate targets at different stages (e.g., Phase I vs. commercial) and different targets (e.g., EGFR vs. Claudin 18.2) to reduce portfolio volatility by 30%.

(C) Geopolitical Risk Response Strategies

- Supply Chain Redundancy

- WuXi Biologics builds dual backup production bases in Singapore and Ireland, ensuring 70% capacity under unilateral sanctions.

V. Frontier Directions: Alpha Mining in Next-Gen Innovative Drugs

-

Industrial Breakthrough of AI-Driven Drug Discovery

- Recursion Pharma's AI discovery platform shortens target validation from 6 years to 2 years, with pipeline count growing 200% annually.

-

Spatial Biology-Driven Precision Therapy

- 10x Genomics' Visium technology enables single-cell resolution of tumor microenvironment, guiding bispecific antibody development with 3x higher success rate.

-

Synthetic Biology Reshaping Production Paradigm

- Ginkgo Bioworks' cell programming platform reduces antibody production costs by 80%, disrupting traditional CMC processes.

BeiGene

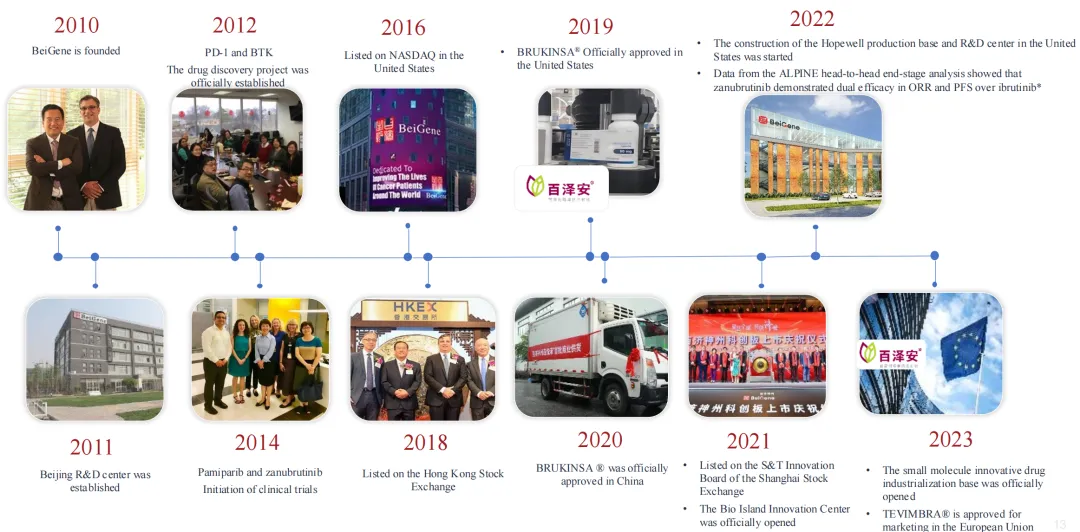

I. Company Development

On February 2, 2016, BeiGene (stock code BGNE, later changed to BeOne, code ONC) went public on Nasdaq at $24 per share, issuing 6.6 million shares and raising $182 million. In a March 2018 follow-on offering, it raised another $758 million. In August 2018, the company completed a secondary listing on the Hong Kong Stock Exchange, raising $903 million. In 2019, Amgen acquired a 20.5% stake in BeiGene for $2.7 billion and gained a board seat. In return, BeiGene obtained commercialization rights to three Amgen drugs (Xgeva, Kyprolis, Blincyto) and 20 other pipeline drugs, committing up to $1.25 billion in R&D for these drugs.

II. Scientific Research Capability

R&D Investment: In Q4 and full year 2021, R&D expenses were $430.5 million and $1.5 billion, respectively, compared to $355.5 million and $1.3 billion in the prior year. BeiGene is currently the Chinese innovative drug company with the highest R&D spending.

2.1 Research Achievements:

- Brukinsa (zanubrutinib): A small-molecule BTK inhibitor for various hematologic malignancies. It received FDA and NMPA approval, becoming the first Chinese innovative drug to go global and BeiGene's profit core. According to Frost & Sullivan, the global BTK inhibitor market will reach $20 billion by 2025; China's BTK inhibitor market is expected to grow to RMB 13.1 billion by 2025. In H1 2022, Brukinsa sales exceeded RMB 1.5 billion.

- Tevimbra (tislelizumab): An anti-PD-1 antibody for various solid tumors and hematologic malignancies. It has been included in the医保 negotiation list, aiming for volume-for-price exchange, and is partnered with Novartis for overseas sales. According to Frost & Sullivan, the global PD-1/PD-L1 monoclonal antibody market is expected to reach $62.6 billion by 2025; China's market is expected to reach RMB 51.9 billion by 2025. In H1 2022, Tevimbra sales exceeded RMB 1.2 billion.

- Pamiparib: A selective PARP1 and PARP2 small-molecule inhibitor. According to Frost & Sullivan, the global PARP inhibitor market is growing rapidly, reaching $12.3 billion by 2025; China's market is expected to grow to about RMB 14.7 billion by 2025.

Collaboration Products and Clinical-Stage Self-Developed Drugs: Include ociperlimab (anti-TIGIT mAb), BGB-11417 (Bcl2 small-molecule inhibitor), BGB-A445 (OX40 agonist antibody), BGB-15025 (HPK1 inhibitor), and 11 other products.

Additionally, through a strategic collaboration with Novartis, BeiGene obtained rights to promote five Novartis oncology drugs in designated regions in China: Tafinlar (dabrafenib), Mekinist (trametinib), Votrient (pazopanib), Afinitor (everolimus), and Zykadia (ceritinib).

2.2 Manufacturing Bases:

- Suzhou: A multi-functional industrialization base covering over 13,000 sqm, producing small-molecule clinical and commercial drugs, with an annual capacity of 1 billion tablets/capsules and 2 × 500L bioreactors for biologics.

- Guangzhou: A world-class biologics manufacturing base covering about 158,000 sqm, primarily for large-molecule biologics. After expansion, total capacity is expected to reach 64,000L.

- Hopewell, New Jersey: A new manufacturing and clinical R&D center on 42 acres, with initial construction including ~400,000 sqft of commercial biologics production space, clinical R&D center, and office areas.

- Beijing R&D Center: Includes a pilot-scale manufacturing base for non-clinical and clinical trial materials for small-molecule candidates.

III. Capital Operations

3.1 Founding Team:

- Wang Xiaodong, a dual academician of the Chinese Academy of Sciences and the US National Academy of Sciences.

- John Oyler, a business talent. Starting with Biopharma, R&D funds were almost entirely provided by capital, backed by star venture capital and star founding team.

3.2 Business Model (Moat):

Starting with globalization, BeiGene is currently the only Chinese company with global commercialization capabilities. Its core competitiveness lies in the world's most advanced molecular targeted drugs and immuno-oncology drugs. Focusing on the most cutting-edge targets and therapies, with sustained large-scale capital investment and a strong R&D team, its innovation capability is far ahead and difficult to imitate or surpass.

3.3 Revenue Analysis:

From the above statements, BeiGene's revenue growth is significant, but due to increased R&D and sales expenses, coupled with weakened external demand, net profit remains sharply reduced.

3.4 Commercialization:

Unlike Big Pharma, BeiGene does not have particularly strong sales channels. As the only innovative drug company listed on Nasdaq, A-shares, and H-shares simultaneously, it has strong financing capabilities. BeiGene's innovative drug R&D requires a high-investment model with continuous financing.

BeiGene entered global strategic collaborations with Bristol-Myers Squibb (2017), Amgen (2019), and Novartis (2021). The Amgen deal was the largest in terms of transaction value and number of products/pipeline drugs between a global pharma and a Chinese biotech; the Novartis deal had the highest upfront payment for a Chinese drug licensing deal.

3.5 Valuation Model:

High investment, high risk; future revenue growth is rapid (low base, strong explosive power).

IV. Valuation and Stock Price Analysis

With a strong global track record, BeiGene has a higher median EV/Sales than Chinese peers. From its 2021 peak, BeiGene's valuation has fallen from ~20-30x EV/Sales to 6x, due to potential geopolitical issues. By 2028, EV/Sales is expected to reach 2.9x, in line with peers, although peers like Innovent have not yet succeeded outside China. Although BeiGene's CAGR is relatively low compared to peers, its revenue trajectory has high certainty given its drug track record. BeiGene recognizes that incremental gains from its pipeline and market sentiment may refocus on its long-term potential.

Peer Comparison

BeiGene's revenue surged in 2023, driven by the maturity of core products Brukinsa and tislelizumab, especially Brukinsa becoming a leading drug for mantle cell lymphoma.

Although still loss-making, the clear improvement indicates that revenue is starting to cover some costs. As product sales mature further, profitability will strengthen.

BeiGene's liquidity risk is also increasing. Declining current assets weaken the liquidity buffer. Increased accounts receivable raise collection risk. Higher inventory brings stockpile and turnover pressure.

BeiGene's improved profitability in 2023 demonstrates successful cost control and market pricing strategies, showcasing its strength in this area. Its R&D costs remain high.

BeiGene's R&D investment far exceeds that of pharma peers, indicating its emphasis on new drug development, meaning it is more likely to develop new drugs and better win the market.

Liquidity Ratio Analysis

BeiGene's working capital fell 35.9%, and the current ratio dropped to 2.32, slightly below the industry standard of 2.5-3.0, but still within a reasonable range. This short-term liquidity sacrifice can support long-term growth. Inventory remains high, potentially tying up capital and increasing impairment risk. Compared to Hutchison China MediTech (HCM), BeiGene has larger current assets but lower inventory and operational efficiency.

Solvency Ratio Analysis

BeiGene's debt-to-asset ratio rose from 31.3% to 39.1%, indicating increased reliance on debt financing. While supporting growth strategy, it also carries financial risk. TIE improved to -10.4, but still insufficient to cover interest. Free cash flow improved but remains negative, potentially leading to financial pressure. HCM outperforms BeiGene in all these metrics.

Profitability Ratio Analysis

BeiGene's gross margin rose from 79.8% to 84.5%, reflecting cost control and pricing advantages. All profitability indicators improved significantly. However, negative margins show profitability has not yet been achieved; all profitability indicators except gross margin lag behind HCM.

From the table, BeiGene's profitability is growing strongly, with 50% of business in the US and 38% in China.

From the table, BeiGene's R&D spending is significantly higher than competitors, indicating stronger research capabilities.

BeiGene Stock Price Trend Analysis (Forecast as of End 2024)

As of now, ONC's stock price peaked at $287.88 before pulling back; BeiGene's H-share peaked at HK$174.8 before pulling back.

References:

- Tencent. (2025, February 26). Market over 1.1 trillion! Multiple innovative drug companies survive 'pain period' and start to profit; financing ecology improving? Pharmaceutical bottoming series. https://new.qq.com/rain/a/20250226A08KQ400

- Tech Planet. (2024, October 10). Innovative drug market trend analysis. https://www.taodocs.com/p-1118219837.html

- Securities Market Weekly Market Number, Beijing. (2024, October 29). Innovative drug investment outlook positive;医保 negotiations and policy support send positive signals. https://www.163.com/dy/article/JFMD2OCA05199FB7.html

- Toutiao. (2024, July 24). Directions to watch in the innovative drug industry. https://www.toutiao.com/article/7395224527208202790/

- China Business Intelligence Network. (2024, August 30). 2024 China innovative drug industry market prospect forecast research report (abbreviated). https://www.163.com/dy/article/JAR1QMCI05198SOQ.html

- Tencent. (2025, February 27). Bad news exhausted; innovative drug trillion market ceiling opens. https://new.qq.com/rain/a/20250227A08QBE00

- Tencent. (2025, March 2). Innovative drug industry observation: Global R&D participation deepens; commercialization accelerates. https://new.qq.com/rain/a/20250302A04CZN00

- BeiGene. (n.d.). BeiGene official website. https://www.beigene.com.cn/

- Bloomberg

Risk Warning: The views in this article are for reference only and do not represent any investment advice. The market carries risks; invest with caution.

Interested? Click to follow!

专注投资分析、市场洞察与资产配置。不追短期波动,只理解真正驱动长期回报的东西。