Several key economic data releases this week shed light on the current state of the US labor market and their implications for rate cut expectations this year.

The data includes:

- Wednesday: JOLTS job openings, ISM Manufacturing PMI

- Thursday: ADP employment data, Markit PMI

- Friday: Unemployment rate, Nonfarm payrolls, ISM Services PMI

Data showed November JOLTS job openings edged down to 8.79 million, slightly below October's 8.85 million. This reflects a labor market that is cooling but still healthy. The ratio of job openings to unemployed workers rose from 1.3 to 1.4, meaning there are 1.4 jobs for every unemployed person, indicating plenty of jobs available. Because the unemployment rate fell (from 3.9% to 3.7%), the ratio increased, signaling fuller employment.

By sector, transportation and utilities saw the largest decline (-128k), followed by leisure and hospitality (-78k). The biggest increases were in wholesale trade (+63k), construction and retail trade (+40k). A decline in JOLTS openings doesn't necessarily indicate weakness—it could be due to filled positions or canceled openings due to insufficient demand. The latter signals industry weakness. Generally, only when business volume increases or is expected to increase do firms post new openings. So the expansion in durable goods manufacturing (+21k) and construction—both interest-rate-sensitive—reflects economic strength and reinforces soft-landing expectations.

Overall, the labor market cooling further reduces inflation (via wages), while job growth in construction and durable goods eases near-term economic concerns.

Data showed the US Manufacturing PMI at 47.4, slightly above expectations (47.2) and November's 46.7, but still in contraction territory, marking 14 consecutive months of contraction. New orders, a proxy for future demand, fell further from 48.3 to 47.1, also in contraction for 16 consecutive months. Production rebounded from 48.5 to 50.3, entering expansion. Employment improved from 45.8 to 48.1. The prices index contracted for the 8th straight month, dropping sharply from 49.9 to 45.2, further signaling easing inflation.

The ISM survey chair noted:

- Manufacturing continued to contract in December

- Respondents maintained production but continued layoffs

- Only 1 of 17 industries (primary metals) had PMI in expansion

- Machinery, petroleum & coal, and electronics had PMI below 45

- 84% of manufacturing GDP is contracting

Despite weak data, business confidence was surprisingly optimistic, with many industries reporting signs of demand recovery and expecting 2024 to be a strong year.

In summary, while manufacturing continues to contract, respondents are optimistic about the future. We need to monitor data to see if recovery materializes. Fed rate cuts remain uncertain, and manufacturing recovery requires more concrete evidence.

Data showed 164k new jobs added in December, beating expectations of 130k and up from 101k in November. Goods-producing: +9k (construction +24k, manufacturing -13k, natural resources -2k). Services: +155k (leisure & hospitality +59k, education & health +42k, other +22k).

On wages, job stayers saw wage growth slow (5.6% to 5.4%), while job changers' wage growth fell from 8.3% to 8.0%—a key sign of labor market cooling. ADP's economist said: "We are returning to a pre-pandemic labor market, where wage growth no longer threatens inflation."

Overall, the strong ADP data confirms the US economy's resilience, but the nonfarm payrolls data below is more important.

Data showed the US added 216k jobs in December, well above the expected 170k and the downwardly revised 173k in November. The unemployment rate held at a low 3.7%.

By industry, economically insensitive sectors like healthcare & social assistance (+59k), government (+52k), and leisure & hospitality (+40k) led gains. Transportation & warehousing saw the largest decline (-23k). The report noted that average monthly job gains in 2023 were 225k, down from 399k in 2022, indicating the labor market, while resilient, is steadily cooling and supply-demand is rebalancing.

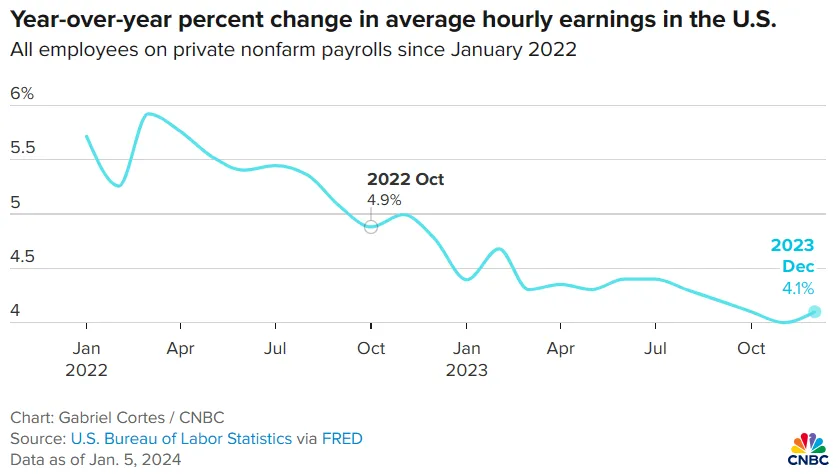

But wages remain a concern. Data showed average hourly earnings rose 0.4% month-over-month, above the 0.3% expected, and 4.2% year-over-year, above the 3.9% expected. The wage trend has not yet reached the Fed's target level; to keep inflation at 2%, wage growth needs to be around 3%. One month's data doesn't confirm a wage rebound, but it breaks the downward trend since mid-year, so continued monitoring is needed.

Overall, the data shows that inflation can decline even with a strong economy, reducing the threat of a strong economy reigniting inflation. Only persistently rebounding inflation would threaten markets. So we need to keep an eye on inflation data for any signs of a reversal that could affect rate cut expectations and the FOMC's decision.

Data showed the December Services PMI at 50.6, below expectations of 52.6 and November's 52.7. The new orders index, a proxy for future demand, fell from 55.5 to 52.8. The business activity index rose from 55.1 to 56.6. The employment index plunged from 50.7 to 43.3. The report noted that layoffs in professional services and human resources are intensifying as companies try to cut costs amid weak demand and economic uncertainty.

Overall, this data was a boost for markets. The PMI shows services slowing but not contracting. The sharp drop in employment is not concerning given the strong nonfarm payrolls, and it actually helps control services inflation, boosting investor optimism. In the last Fed minutes, it was noted that while goods inflation is declining, services inflation remains high, requiring further labor market rebalancing in services to ease inflation. One caution: the low employment index levels are reminiscent of past recessions. If subsequent data remains weak, it could increase recession uncertainty.

专注投资分析、市场洞察与资产配置。不追短期波动,只理解真正驱动长期回报的东西。